Most people understand that a mortgage is a loan from a bank (or other lending institution) in exchange for property. The actual processes of the home loan are quite a bit more complex than that. In fact, even paying back the loan is a little more complex than when paying off other types of loans. For the borrower, it is not a real big deal. The lender has to do most of the work, but it is still important to know what to expect.

Before walking into the lender’s office you should make sure to have things in order. Bringing pay stubs for the last few months, and tax records for the last two years will help facilitate the process (in fact, call the lender first and ask them what they want to see). Make sure you understand your credit score because it will help to eliminate any surprises. After the application is filled out, the lender must decide if you are an acceptable risk. Computers have sped up the underwriting process considerably, and make for a much simpler job. Within a matter of seconds your income, credit score, and assets will be calculated and the lender can let you know how much they are willing to lend and at what interest rate. After you have found a home and decide to finalize the loan, the lender has quite a bit of behind the scenes work to do. When it is issued, your lender will either service the loan, or sell it off to another company for servicing. You have no control over this process; your job now is to make regular payments.

Those payments will consist of four parts. Principal, interest, taxes, and insurance (PITI) all go into the monthly payments. If you put less than 20% down on the house, then you will also be required to pay for Private Mortgage Insurance or PMI.

Principal

The principal on the loan is the amount owed. The loan is designed so that each payment made will bring the total amount down a little. This means that every payment you will pay less in interest and more in principal until at the end of the term (usually 30 years) the entire principal has been repaid.

Interest

Interest is calculated based on the amount remaining on the loan. Since every payment will bring the amount remaining down, the portion of the payment that goes to interest will go down. But the payments always remain the same, so the amount that goes toward principal increases.

Taxes

Taxes vary by locality, and almost always increase in price over time. Most lenders create an escrow account in the loan and pay the taxes when they come due. This saves the homeowner the trouble of coming up with a lump sum of money to pay for their taxes. It is a free service provided by the lender.

Insurance

Insurance varies by company, house, and location. Since the lender wants to make sure the asset collateralizing the loan is protected, they offer a service of paying for the insurance out of that escrow account. Rather than risk the borrower missing a payment, the lender takes care of it.

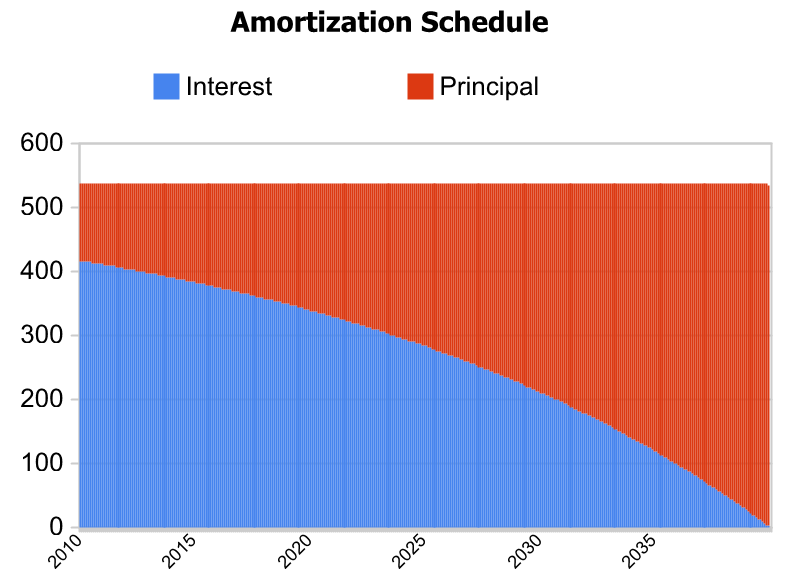

Without taxes or insurance the monthly payment throughout the lifetime of the loan would stay the same. During the early years of the loan, you will end up paying more toward interest and less toward principal. But as the remaining balance drops, your payments will go more toward principal and less toward interest. Here’s a graph that shows the correlation.

{kind=link}

These loans are not short term commitments. By being prepared and budgeting wisely you can make sure that you are not getting in over your head. Knowing what is to come will eliminate surprises, and allow you to enjoy the home that you purchased.

Did you enjoy this article? If so sign up for our daily newsletter so you can stay on top of every personal finance topic we cover. Also check us out of Facebook, Twitter and Google+.

Good to know! I’ll definitely remember all this when it’s time for me to buy my first place.

It’s shocking how often most people don’t realize there are other payments involved in a mortgage (i.e. taxes and insurance). Those two things add quite a bit to the monthly payment and could easily strap people.

Great basic post on mortgages. A home purchase also happens to be the biggest leverage most of us take on in our lives.

I’d like to add that taking a look at your credit report to

see if there’s anything out there that might flag you as a bad credit risk is

another thing you need to do, as well as learning what the property taxes might

be like in the area you might be looking to move to. Sometimes you find that

property taxes will cost you more than your mortgage will, and in some states

it’s your first time home buyer your escrow has to be paid at the same time as

your mortgage up until the point you’ve paid at least 75% on what you owe on

your home.